Most deals don’t die at the negotiating table. They die in the data room — weeks after a buyer and seller shook hands.

Due diligence is the part of the sale process that most business owners underestimate — until they’re in the middle of it. A buyer has signed a letter of intent, you’ve told your accountant, maybe even started mentally planning your next chapter. Then the buyer’s team starts pulling documents.

What they find in those documents will either confirm the deal or unravel it. And the frustrating truth is that most of the surprises that kill transactions aren’t fatal business problems. They’re fixable issues that sellers never got around to fixing because no one told them they needed to.

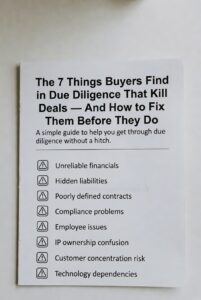

Here are seven of the most common deal killers we see in due diligence — and what you can do right now to get ahead of them.

1. The Financials Don’t Match the Story

This is the most common reason deals fall apart. A seller says the business does $800,000 a year and generates strong cash flow. Then the buyer’s accountant looks at three years of tax returns and sees $480,000 in revenue and a modest profit. The gap is usually explainable — cash transactions, owner add-backs, personal expenses run through the business — but it’s not documented.

Buyers don’t walk away because the numbers are messy. They walk away because they can’t verify the story. If you can’t support your claimed earnings with paper, a buyer will either reprice dramatically or exit the deal entirely.

The fix:

Work with your accountant or a business broker to prepare a formal recast P&L before you go to market. Document every add-back with a clear explanation and backup. A buyer who can follow the math will pay for it.

2. Lease Issues the Seller Didn’t See Coming

The business is tied to a location. The location is tied to a lease. And the lease — in a surprising number of small business sales — contains language the seller has never read closely.

Common surprises: the lease is non-assignable without landlord consent, it expires in less than 18 months with no renewal option, or the landlord has a co-tenancy clause that could affect operations after a change of ownership. Any of these can stop a deal cold, especially when a buyer is financing the acquisition through an SBA loan. Lenders want lease security.

The fix:

Pull your lease and read it before you list. Identify the assignment clause, the expiration date, and any landlord consent requirements. If there’s a relationship issue with the landlord, address it early — not after a buyer is already committed. A transferable lease with years of runway is a genuine value asset.

3. Revenue Concentration

A buyer doing diligence will map your customer revenue by account. If one client, one referral source, or one fleet relationship represents more than 20 to 25 percent of sales, that’s a concentration problem. Lenders often won’t finance a deal where a single customer could walk and take a third of the revenue with them.

This is especially common in service businesses — contractors, staffing firms, specialty shops — where long-term relationships with a few big accounts can quietly become a liability.

The fix:

The honest answer is that revenue concentration takes time to fix, which is why you want to identify it early. If you’re 18 to 24 months from a sale, start diversifying deliberately. Add new accounts. Reduce the largest client’s share. If you’re already in a deal, be transparent about it and work with your broker on how to structure the risk — earnouts, seller financing, or transition agreements can sometimes bridge the gap.

4. Undisclosed Liabilities

These range from the innocent to the serious. Unpaid payroll taxes. A lawsuit that settled but left a judgment on record. An equipment lease the seller forgot was in the business’s name. A personal guarantee on a line of credit that’s attached to an asset the buyer thought was unencumbered.

Buyers run UCC searches, lien searches, and litigation checks. What they find that the seller didn’t mention — even if it’s technically manageable — triggers a trust problem. Once a buyer starts wondering what else wasn’t disclosed, deals get complicated fast.

The fix:

Do your own diligence on your own business before a buyer does. Pull a credit report on the business entity. Check for open judgments or liens. Review every financial obligation that’s in the company’s name. Surface anything questionable and address it proactively. Disclosure with context is far less damaging than discovery without it.

5. Key Person Dependency

This one is subtle because it doesn’t show up in the financials. The business looks profitable, the revenue is consistent, the customers are happy — but everything runs through one person. You. If you’re the primary relationship manager, the main technician, the only one who knows the vendors, or the face of the brand, a buyer is buying a business that may not survive the transition.

SBA lenders often require the seller to stay on for a transition period precisely because of this risk. But a year of seller involvement doesn’t solve the structural problem. Buyers who are sophisticated will price it in, or pass.

The fix:

Start delegating with intention, ideally 12 to 24 months before a sale. Document your processes. Empower your managers. Let employees own relationships with key accounts or vendors. A business that runs without the owner is worth more, sells faster, and closes cleaner.

6. Licensing, Permits, and Compliance Gaps

Depending on the industry, a business may require specific licenses that are tied to the individual owner rather than the entity. In some cases, those licenses aren’t easily transferable. In others, the business has been operating under an expired permit it never got around to renewing.

This comes up regularly in trades businesses, food service, childcare, healthcare-adjacent services, and any industry with regulatory oversight. A buyer who discovers a compliance gap during due diligence doesn’t just see a paperwork problem — they see potential liability and transition risk.

The fix:

Audit your licensing and permit status before you list. Know what’s transferable, what requires re-application, and what might require a licensed individual to remain involved post-closing. Your broker and your attorney should be part of this conversation early.

7. Inconsistent or Missing Business Records

Buyers ask for a lot of documents. Three years of tax returns, monthly P&Ls, accounts receivable aging reports, employee records, vendor contracts, equipment lists, insurance certificates. When sellers can’t produce them — or produce versions that conflict with each other — the due diligence process stalls.

A stalled due diligence process is a dangerous place to be. Buyers lose momentum. Financing timelines slip. Attorneys start running up hours. And the longer a deal drags, the more chances there are for it to fall apart over something unrelated to the actual business.

The fix:

Build a simple data room — a folder, digital or physical — where your key business records live and stay current. Tax returns, financial statements, contracts, and licenses should be organized and accessible. When a buyer asks for something, you should be able to produce it in 24 hours. Responsiveness and organization signal that you run a tight operation. That matters.

The Common Thread

Look at that list again. None of these issues are business-ending by nature. A lease can be renegotiated. Financials can be recast. Processes can be documented. Customer concentration can be diversified. Most of these problems are entirely solvable — but only if you know about them before a buyer does.

The sellers who close deals at strong prices are rarely the ones with perfect businesses. They’re the ones who did the work to understand their vulnerabilities and address them honestly. That preparation is what turns a listing into a closing.

If you’re thinking about selling in the next one to three years, the smartest thing you can do is start the conversation now — before any of these issues become someone else’s leverage.

Michael Shea represents the Tampa Florida Transworld office. In business since 2005, he has established a reputation as a trusted business broker across Florida’s key markets- from Tampa to Orlando, Melbourne, and more. Over the past two decades, Michael and his team have closed over $1 Billion in sold business volume and presided over more than 450 transactions. His credentials include the IBBA Certified Business Intermediary®, and most recently, the prestigious Certified Exit Planning Advisor® (CEPA) credential.