Selling a business is often harder than starting one. To turn your years of “sweat equity” into a life-changing payout, you have to stop thinking like an owner and start thinking like a seller. Here is how to do it:

1. Sell While You’re Winning (Avoid the “Bad D’s”)

Don’t wait for a crisis to exit. Most owners are forced into a sale by the “Bad D’s”: Death, Divorce, Disagreement, or Disability. When you have to sell, you lose all your leverage.

-

The Goal: Commit to the sale while the business is thriving and your life is stable.

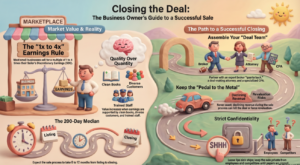

2. Embrace the “Multiple” of Reality

Valuation isn’t a guessing game; it’s anchored in market data. “Main Street” businesses (under $1M in earnings) typically sell for 2.0x to 2.8x their Seller’s Discretionary Earnings (SDE).

-

The Anchor: Banks won’t fund a deal if the cash flow can’t cover the debt. Your price is effectively capped by what a lender is willing to underwrite.

3. Loose Lips Really Do Sink Ships

The moment employees, customers, or competitors find out you’re selling, value begins to leak.

-

The Strategy: Use “strategic ambiguity.” (e.g., A niche knife distributor marketing itself as a “camping equipment” business).

-

The Rule: No one should know about the sale until the wire transfer hits your account.

4. Keep Your Foot on the Gas Until the End

Many sellers “coast” once they sign a Letter of Intent (LOI). This is a fatal mistake. Lenders perform “show time” due diligence and will demand a P&L for the 30 days immediately preceding the closing.

-

The Risk: If revenues dip in the final month, the buyer will re-trade the price lower or the bank will pull the funding entirely.

5. Watch Out for the “Landlord Veto”

If you rent your space, your landlord is a silent partner in your exit. Most SBA loans require a 10-year lease. If the landlord won’t assign the lease or grant an extension, your deal is dead.

-

The Decision: Decide early if you are selling the real estate or becoming your buyer’s new landlord.

6. Stop Playing “Tax Games” with Your Books

Aggressive tax strategies—like hiding cash or over-expensing personal travel—might save you a few dollars in April, but they’ll cost you hundreds of thousands at the closing table.

-

The Reality: If you can’t prove what you made on paper, you can’t prove what the business is worth. Clean, “boring” books lead to much higher sales prices.

7. Hire a Quarterback, Not Just a Risk-Finder

Selling a business is a team sport. You need a “deal-maker” attorney and a broker who can act as the Quarterback.

-

Why a Broker? They are the only ones who can speak to everyone—buyer, seller, CPA, landlord, and lender—to keep emotional friction from derailing the transaction.

The Bottom Line: Success depends on a clear financial story and a mindset ready for the hand-off. If someone offered you a check today, would your books be ready?

Michael Shea represents the Tampa Florida Transworld office. In business since 2005, he has established a reputation as a trusted business broker across Florida’s key markets- from Tampa to Orlando, Melbourne, and more. Over the past two decades, Michael and his team have closed over $1 Billion in sold business volume and presided over more than 450 transactions. His credentials include the IBBA Certified Business Intermediary®, and most recently, the prestigious Certified Exit Planning Advisor® (CEPA) credential. He is also a Florida Licensed Real Estate Broker and Business Brokers of Florida Board Certified Intermediary